Given the recent turmoil at Uber and with all the negative ink being written about its sky-high valuation, people have been doom and gloom about the company’s future (ie: HBR on need to shut Uber)

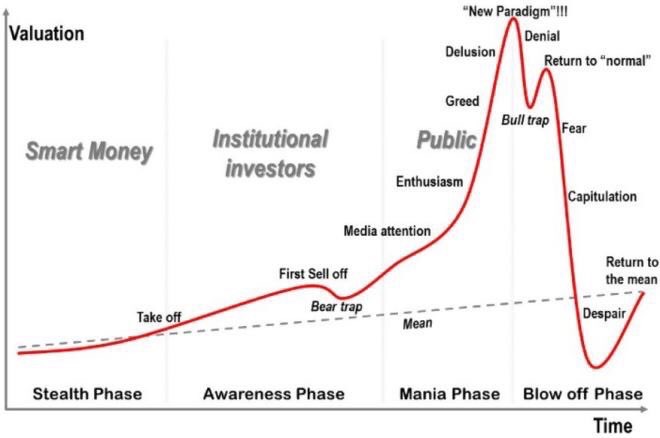

The difficulty to turn a profit combined with the management issues of the last few months has made Uber a classic case study of how start ups’s valuation fluctuates and how hot money tends to follow media attention and public enthusiasm about a company (Theranos went through a very similar flow but with an actual problem with its business case).

The Uber concept is good and it’s monetisation is real. It solves a real life problem and it still has a demand-to-pricing gap that can help to boosts its revenues. It just feels like the market might be catching up to reality and is turning bearish on a company that is going through difficulties. Its expansion plan is still to show signs of sustainability and the pop up in competitors might only exacerbates the worries of investors.

Another threat to Uber is the local competitors popping up left and right. Local population is always going to be more inclined to use their local outlet rather than using an American start-up. Take for example Spain or Cambodia: Cabify and Exnet have the majority of the local market and Uber will have real difficulty eating into that. So unless Uber see real, long-term value in cross-geographical users, it might have to re-think its expansion and its sustainability. However, and I say this as a user, the easiness and safety of the Uber experience is unrivalled. And for a person that travels frequently and that has to taken Ubers in almost ten countries, I am a fan; a big one!

One thought on “A start-up’s valuation life cycle”